Table of Contents

The most crucial ingredient of an automobile-mortgage is arguably the desire level. It specifically influences the dimensions of monthly payments and overall financial loan tenor. Interest rates can even perform a job in the final getting conclusion, highly effective plenty of to override sentimental invest in good reasons these as manufacturer loyalty. It goes with no declaring, consequently, that possible car or truck consumers spend focus to aspects that determine their fascination costs when buying for vehicle-funding possibilities.

A single of this sort of factors is the credit score score. It is essentially a weighted score that tells auto-loan providers how considerably threat they are taking on by dealing with a future borrower. You most possible have a credit report if you have any credit score accounts, these kinds of as credit history playing cards, mortgages or loans. This report then types the foundation for pinpointing your credit rating rating.

It is not an exact measure, but it does lose mild on components these types of as the borrower’s willingness and capacity to company the personal loan. Basically place, the greater your credit history rating, the bigger your odds of securing an car loan with favourable interest charges. This is specially critical these days as we navigate the era of fascination amount hikes and inflationary pressures.

Employing your credit score rating to secure the ideal interest costs

By means of Experian

The total purpose of the credit history score is common. On the other hand, diverse loan companies in diverse sections of the entire world have their own conditions to evaluate an individual’s creditworthiness. When you use for an vehicle mortgage in the US, the loan provider will operate a credit test as aspect of the system. The greater part of the lending institutions use FICO credit scores. This is a 3-digit score assigned to a borrower right after the credit history check out exercising.

It was in the beginning made in 1989 by a knowledge analytics enterprise known as Fair Isaac Corporation. Today, there are a lot of variants of the FICO algorithm (and other scoring versions, for that subject), but they are all aimed at ascertaining the borrower’s capacity to get on credit score.

By means of The Harmony

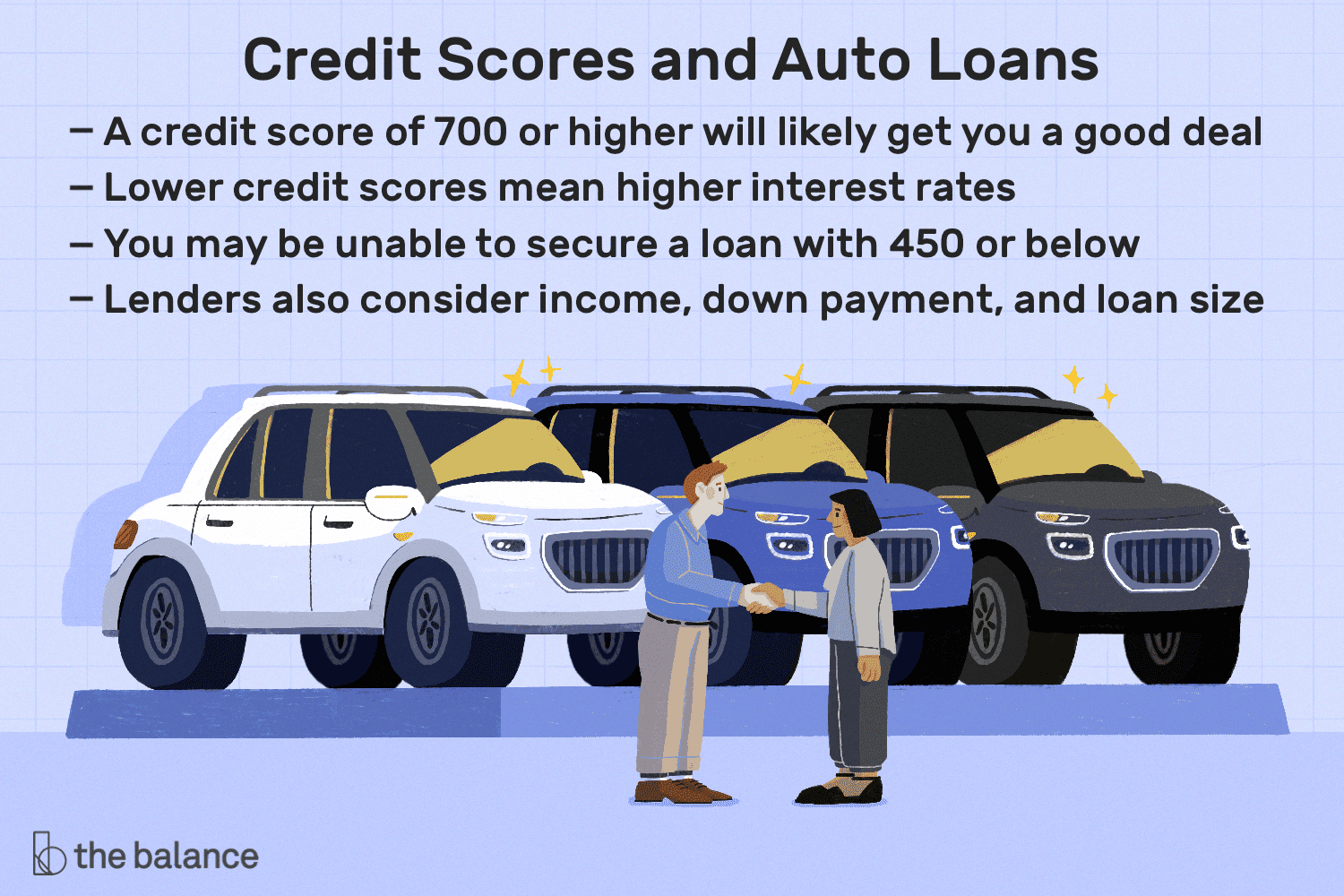

In accordance to the CFPB (Consumer Economic Safety Bureau) Shopper Credit score Panel, there are five various borrower profiles sorted into the next credit rating rating buckets: Super-key (720 & over) Prime (660-719) Close to-prime (620-659) Subprime (580-619) Deep subprime (under 580). A borrower with a score down below 660 can even now protected vehicle financial loans, but they will be much more pricey than a Prime or Tremendous-primary borrower with a rating north of 661. The logic here is that you will want to hold your credit history score as large as achievable to get the greatest deals when browsing for car loans.

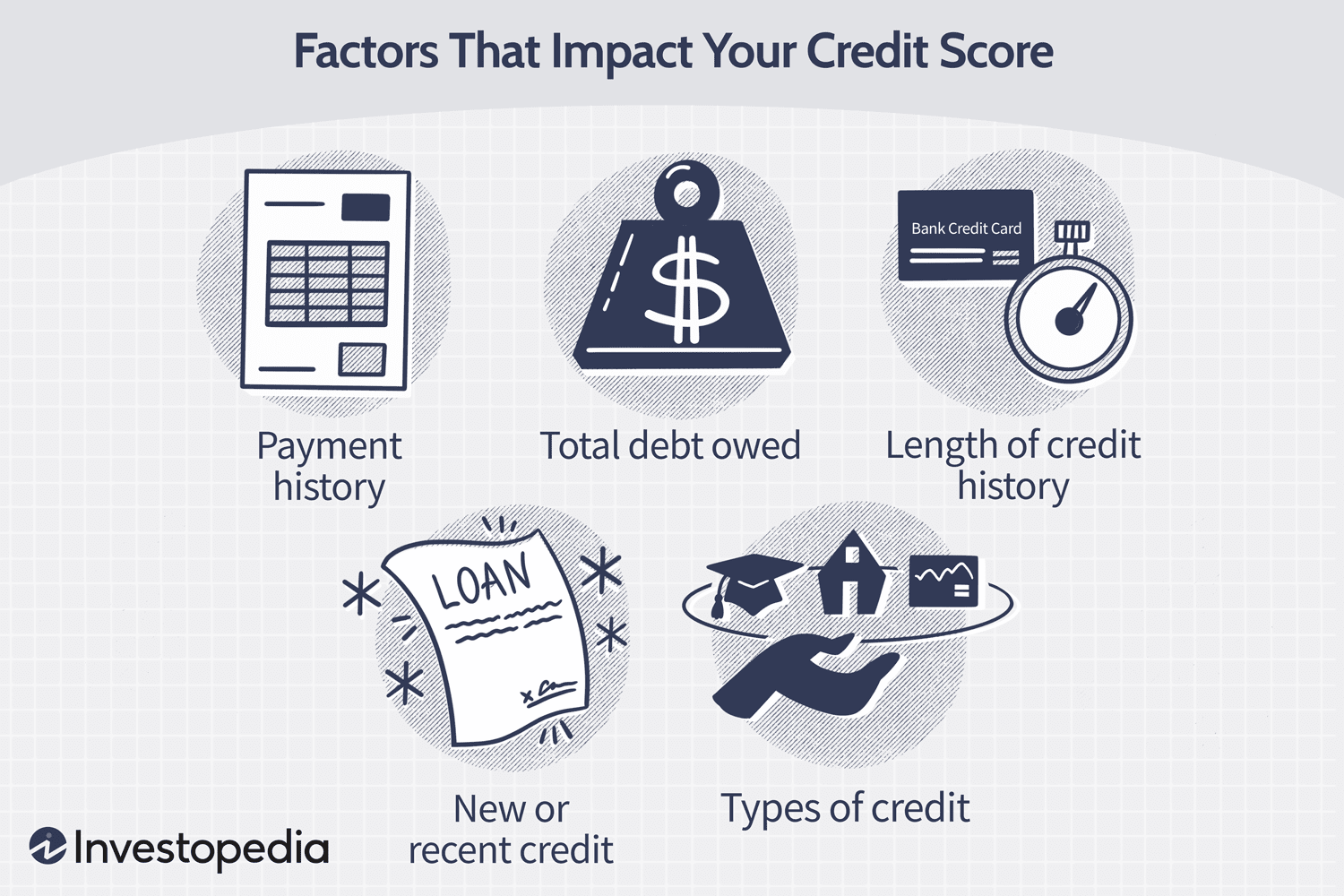

Factors that harm your credit score

By using Investopedia

An superb credit score is the consequence of watchful and deliberate arranging, and understanding the prospective pitfalls can aid the borrower prevent producing missteps that pull down the rating into undesirable territory.

Earning a late payment

Payment background on your credit rating obligations accounts for up to 35% of the FICO rating. In accordance to FICO, a payment that is 30 times late can price a person with a credit history rating of 780 or bigger everywhere from 90 to 110 points. It is important to make payments as at when due and proactively achieve out to the lender if, for any cause, payment will be delayed.

A large personal debt-to-credit score utilization ratio

Credit record is designed by a constant cycle of credit utilization and fork out downs. Nonetheless, you will want to keep an eye on the proportion of your debt load to in general credit rating. The reduce your balances relative to your full available credit history, the much better your rating will be.

Non-utilization of credit rating

On the other hand, no credit score record for an prolonged interval can also adversely influence the borrower’s credit history rating. Loan companies and lenders have absolutely nothing to report to credit bureaus when you never employ your credit score accounts. This tends to make it much more complicated to appraise future mortgage programs.

Individual bankruptcy

Filing for bankruptcy has a person of the most important impacts on your credit rating rating. It can wipe as much as 240 factors from an individual’s rating, and what’s more? A individual bankruptcy report can keep on the credit history historical past for up to 10 a long time.

This listing is by no indicates exhaustive, and other components these kinds of as frequency of credit applications, credit score card closure, cost-offs and refinancing all effect credit score scores in varying levels.

Enhancing your credit score rating

Improving your credit history score will include keeping away from the pitfalls earlier recognized earlier mentioned. Methods these types of as prompt and common bill payments, maintaining a minimal debt-to-credit rating utilization ratio (preferably about 30%), preserving credit rating card accounts open and steering clear of many mortgage apps at as soon as are all methods in the suitable way.

On the other hand, even with all these ‘building blocks’ in position, a excellent credit score score is not instantaneous. It may perhaps get a when to see any enhancement, primarily since unfavorable studies can remain on your credit history heritage for various decades. There is no rigid time frame for credit score score progress as just about every person’s fiscal predicament is one of a kind. In accordance to Forbes, it could acquire any where from a thirty day period to as much as ten many years. Clearly, this is motivated by components these kinds of as the individual’s latest credit history status and quantity of whole exposure.

Securing auto financial loans regardless of credit rating

Via Geotab

A large credit history score will definitely strengthen your prospects of securing automobile funding and locking up the greatest curiosity costs. On the other hand, it is not all doom-and-gloom for potential car or truck consumers with weak scores as they are not solely without the need of possibilities.

Regardless of your credit score rating, hunting all-around and thinking of the numerous funding alternatives is extremely encouraged. It is just like procuring for the car or truck itself an regular purchaser will consider distinct dealerships and negotiate vigorously prior to building the closing determination.

Banking institutions are the classic resources for obtaining a personal loan, but you could be restricting your selections if they are your only consideration. Don’t dismiss alternate lenders. Functioning with 3rd-bash financing companies, these kinds of as finding your automobile mortgage by means of LoanCenter.com, may supply you with favourable desire prices or financing conditions.

It is essential to take note that simply just getting car-bank loan preapprovals (different from genuine financial loan purposes) though purchasing about will not impact your credit history score given that most scoring styles do not handle this as a tough enquiry.

In summary, a weak credit rating score may perhaps push the lowest curiosity rates out of reach. Nevertheless, acquiring quite a few solutions will enhance your likelihood of finding a bundle with an curiosity charge that matches in your spending plan and allow for you to purchase your wanted car or truck.